This Cable Giant Could Be The Smartest Way To Play AI And Power

Prysmian sits right where two trends collide: the scramble to upgrade electrical grids and the even bigger scramble to wire AI. And it’s been in both of Theodora’s data center and power grid upgrade p

My data center and global power grid portfolios have both had a roaring run this year. Demand’s been explosive, and that’s had companies boosting their forecasts, filling their order books, and beating Wall Street’s already ambitious expectations.

That’s the good news.

But it also means that the easy money in the two themes has probably already been made. So over the next couple of months, I’m going to dig into these portfolios and pull out the names that still feel especially important – the companies that remain strategically viable, underappreciated, or just worth exploring.

First up: Prysmian.

It sits right in the overlap between both themes. It’s plugged into the power grid upgrade story through its ties to high-voltage cables and broader infrastructure. And it’s tied to the data center boom through the electrical and connectivity systems that the AI facilities need to function.

Part 1: What does Prysmian do?

Prysmian is the world’s biggest maker of energy and telecom cables and the systems around them. It’s based in Milan and designs, builds, and installs the cables that move electricity and data across the modern economy.

That covers a lot of ground. At one end, you’ve got huge submarine high-voltage direct current cables that link offshore wind farms back to shore. And at the other end, you’ve got the low-voltage building wire running through homes, office blocks, factories, and data centers. Following its acquisition of Encore Wire in 2024, Prysmian became a bigger, more global business with a much stronger foothold in North America.

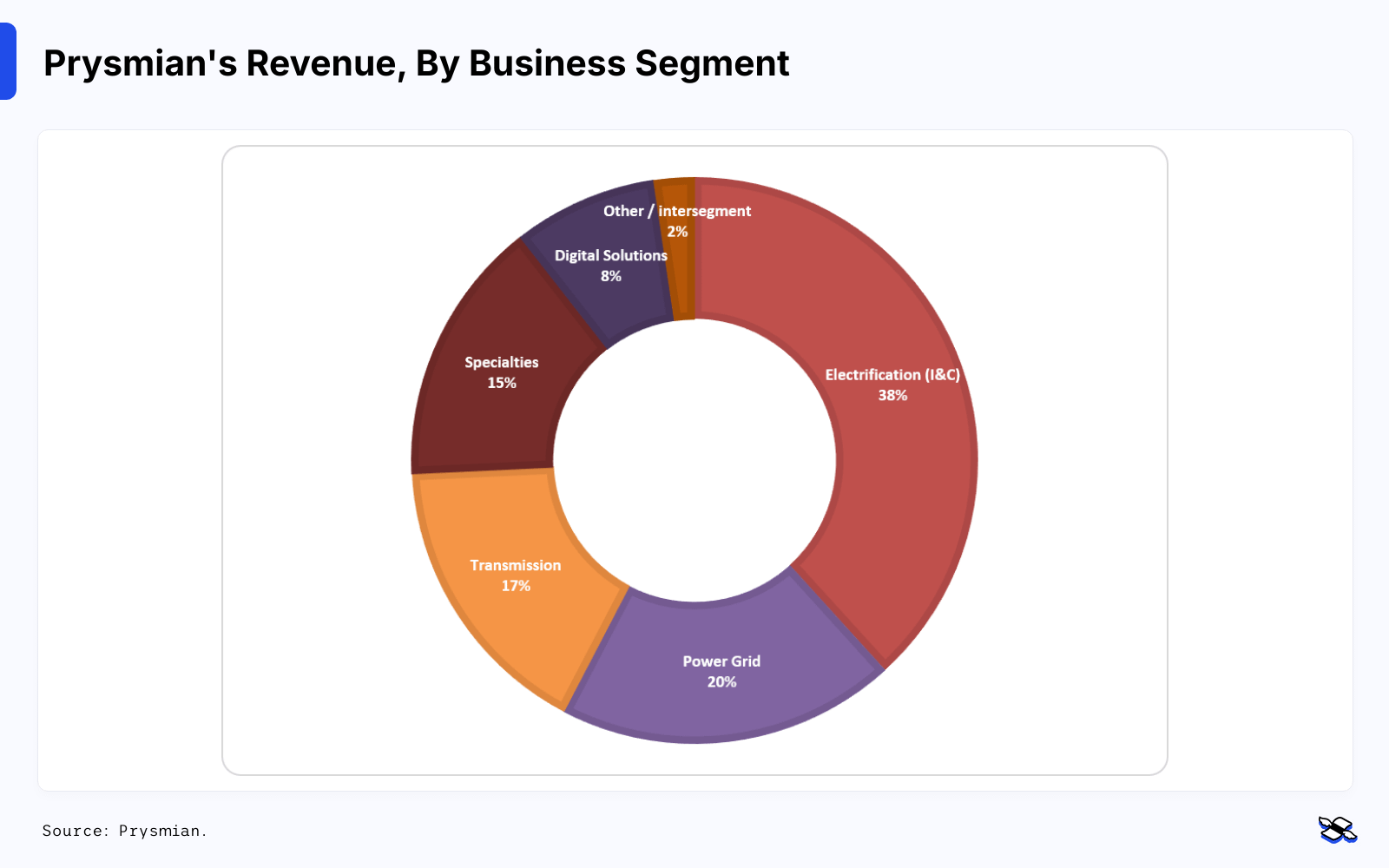

Electrification is Prysmian’s biggest business segment by far. Source: Prysmian.

The company essentially reports across five segments: transmission, power grid, electrification, specialties, and digital solutions.

The biggest by revenue is electrification, which generated 38% of group revenue in 2025. This segment includes industrial cables, building wire, and Encore Wire’s North American residential and commercial low-voltage business. It’s not the sexiest part of the story, but it matters because it gives Prysmian real scale in the US. Thanks to Encore, it’s now the North American leader in copper and aluminum residential and commercial wire. That business sells mainly through electrical wholesalers and big-box distributors like Sonepar, Rexel, Graybar, Home Depot, and Lowe’s.

And that Encore deal brought in more than just extra revenue. It gave Prysmian more control over its own supply chain – what’s generally called vertical integration – including copper rod and PVC compound. It also added a highly automated single-site campus in Texas, and a same-day shipping model that has historically delivered better-than-industry-average service levels. And in a market where copper prices can move quickly and customers care a lot about getting their products on time, that combination of cost control, speed, and strong distribution relationships is a serious advantage.

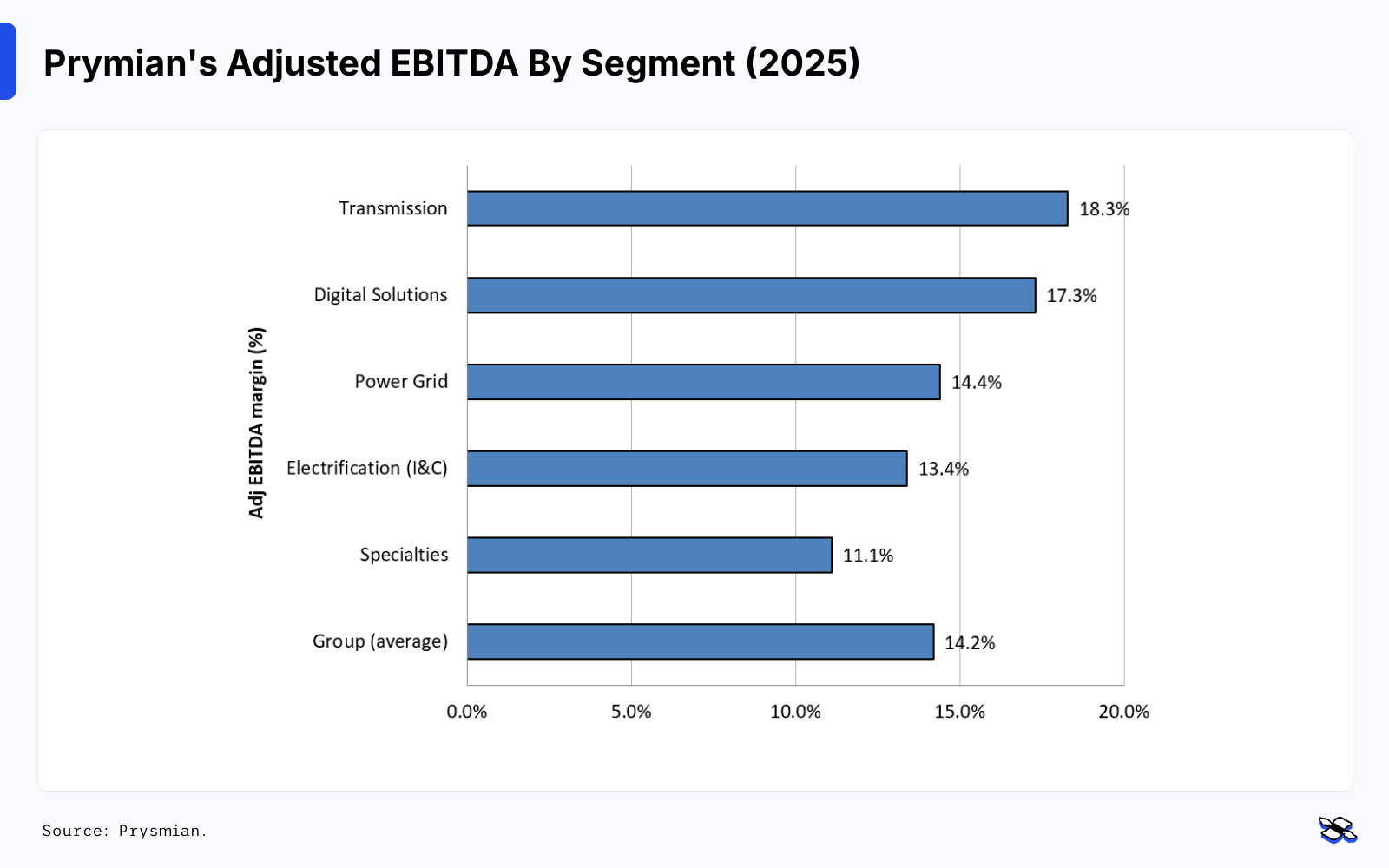

Transmission is the most profitable segment for Prysmian. Here’s a look at each segment based on their adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) margins. Source: Prysmian.

The most strategically exciting segment, though, is transmission.

That’s where Prysmian makes the heavy-duty stuff: long-distance high-voltage and extra-high-voltage land and submarine cables, including the HVDC mega-projects that connect offshore wind farms, islands, countries, and regional grids. HVDC stands for high-voltage direct current – basically the technology used to move huge amounts of electricity over long distances with minimal losses.

Transmission produced €3.3 billion ($3.8 billion) of revenue in 2025, roughly 17% of the group total. It grew 29% organically that year – in other words, from the existing business, not from acquisitions – and delivered an adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) margin of 18.3%. That margin figure meant the segment hit Prysmian’s 2028 margin target three years early.

Even better, transmission ended the year with a record €16 billion order backlog, plus a further €3 billion of identified pipeline, equal to roughly five years of segment revenue visibility.

That kind of visibility is rare – and it’s the kind of thing investors tend to appreciate.

These transmission projects aren’t quick gigs. They usually involve long bidding processes and then take three to seven years to execute. Revenue gets recognized over time as the project progresses, so today’s order book becomes tomorrow’s revenue stream. And customers are typically transmission system operators, national grid companies, and offshore wind developers – names like TenneT, 50Hertz, Amprion, National Grid, Terna, Statnett, alongside RTE, Ørsted, Iberdrola, RWE, EDF Renewables, and Equinor.

Then there’s the power grid segment, which generated a fifth of 2025’s revenue. It’s the part of the company that makes medium- and high-voltage distribution cables for utilities and grid operators. And sure, it’s less spectacular than transmission, but it’s steadier, too. It tends to run on annual framework agreements with utilities, which are usually renewed every two to three years, with monthly orders as customers need product. So it’s more recurring and less project-lumpy – less feast-or-famine – than the big submarine-cable business.

The specialties unit, meanwhile, contributed €3 billion of sales. And this is the grab-bag industrial wing, covering oil and gas, mining, transportation, elevators, and other niche uses for cable. This end of the business offers some helpful diversification, but it’s not a real reason to own the stock.

Finally, there’s digital solutions, the smallest segment at €1.6 billion of revenue, but potentially the most interesting. This business includes optical fiber, telecom infrastructure cables, and connectivity products used by data centers and hyperscalers – the giant cloud companies at the center of the AI buildout. Prysmian has said that it’s close to finalizing long-term framework agreements with hyperscale cloud and AI customers that could be worth more than $5 billion over a few years. And it’s planning to expand its optical-cable capacity by 40% to 50%.

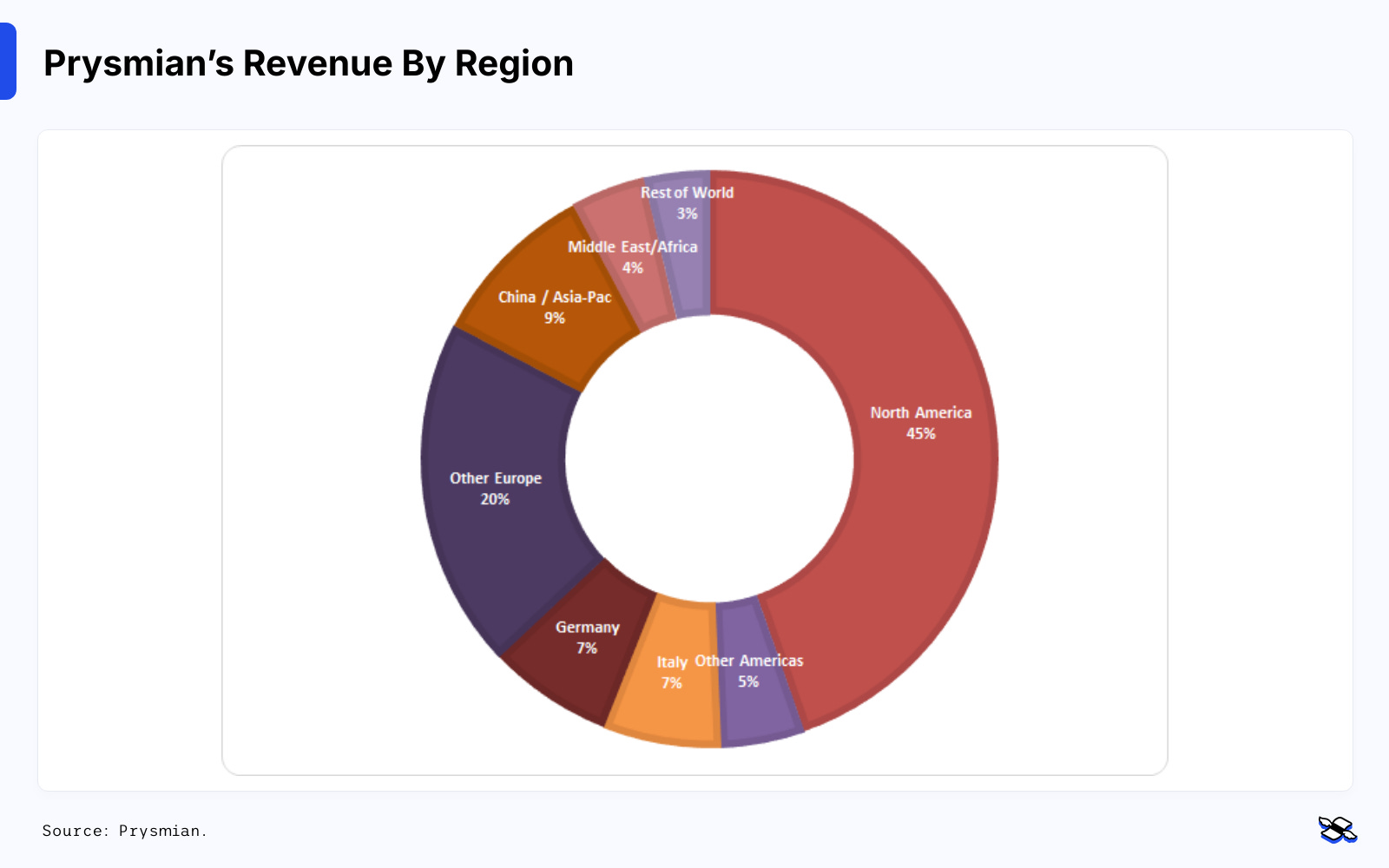

Geographically, Prysmian is nicely balanced: about 50% last year’s revenue came from the Americas, 35% from Europe, and about 15% from Asia, the Middle East, and Africa. Europe still matters a lot for transmission, because of offshore wind and interconnector demand, but the US has become Prysmian’s single biggest country after the Encore acquisition.

Prysmian’s business breakdown has some hefty exposure to North America. Source: Prysmian.

On costs, then, Prysmian is heavily exposed to copper, aluminum, lead, PVC, and other industrial materials. That sounds a little unsettling, until you get into the details. See, most of its commodity risk is managed through contractual pass-throughs – clauses that let the firm pass those higher costs on to customers – and hedging practices that protect against price swings.

In major transmission projects, contracts also tend to include escalation clauses and commodity pass-throughs, though there’s still some leftover risk if forecasts, timing, or hedges don’t line up quite right.