How Our Research Picks Have Held Up: June 2026

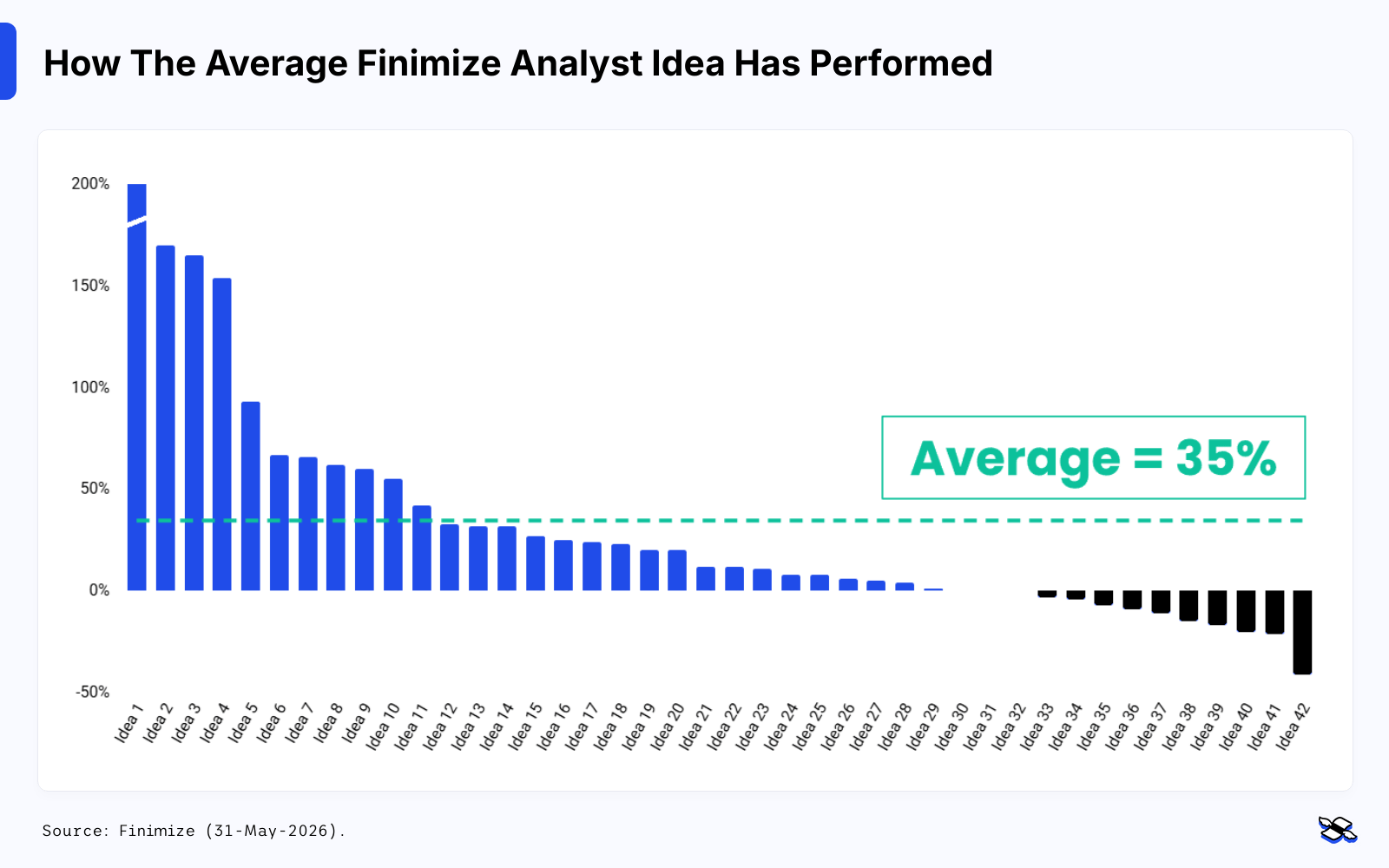

They’re up 35% on average since launch, almost double their benchmarks. Here’s what’s working, what’s been shaken, and what we’re changing now.

Markets have a very direct way of telling you just how smart your ideas are (or aren’t).

So once a month, we go back through our Research investment ideas and see how they’re actually holding up. Every trade is tracked, every number reviewed, and every update is there for you to inspect: the hits, the misses, the slow burners, the character-builders.

Since their launch in October 2024, our ideas have delivered an average return of 35%, beaten their benchmarks by 16 percentage points, and posted a 74% “hit rate” – meaning most of our calls made money.

The average Finimize analyst idea has delivered a 35% return. Source: Finimize.

But it’s a new month, so let’s go analyst by analyst, and get into what worked, what didn’t, and the changes we’re making from here.

Russell: Neoclouds, humanoids, memory, Hormuz, and TransMedics.

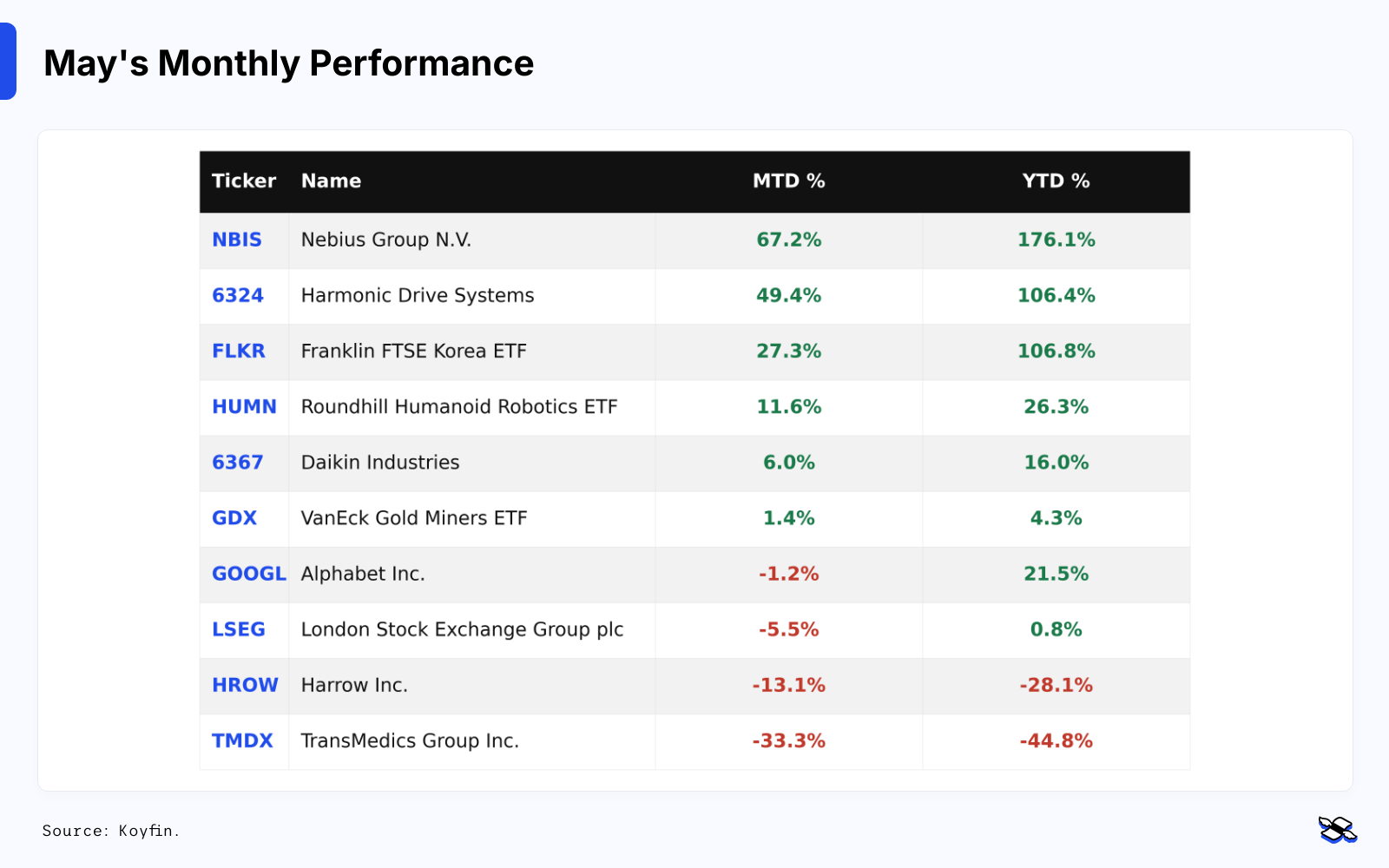

My best picks had a fantastic month. Nebius was up 67% in May, Harmonic Drive was up 49%, and the Franklin Korea ETF was up 27%. All three continue to drive performance, and all three have more than doubled since the beginning of the year.

Monthly performance of open (and now one closed) ideas in the Finimize Portfolio. Source: Koyfin.

Nebius

Nebius has now climbed 170% this year, closing the month at $220. The latest jump happened after the neocloud company reported very strong earnings, which I wrote about here. The main takeaway is simple: Nebius keeps doing what it said it would do and rising to meet the AI boom’s insatiable demand.

Last July, the stock was trading around $50. Back then, I laid out a very optimistic scenario in which Nebius could eventually build a gigawatt (GW) of data-center capacity. That kind of power could support around $10 billion in yearly revenue, using a ballpark assumption of $10 in annual sales per watt.

At the time, it seemed ambitious. The company was aiming to have just 100 megawatts (or 0.1 gigawatt) by the end of 2025.

Under that 1 GW scenario, I estimated that Nebius could eventually rake in around $10 billion in revenue and $2.5 billion in operating profit, or earnings before interest and taxes (EBIT). I used a 25% EBIT margin to come to those figures, which was definitely on the optimistic side, and then I applied a valuation measure of 16x its enterprise value (that’s the EV-to-EBIT multiple), and came up with a possible market value of $40 billion.

That sounded like a lot, sure. But the firm’s market cap just hit $57 billion, quadruple what it was a year ago. And the wildest part of this is that it looks like the company is just getting started.

Last month, Nebius said it had already contracted over 3.5 GW, beating the 3 GW target it had set for the end of 2026. It’s now aiming to bring more than 4 GW of contracted capacity online by year-end.

Using the same rough math, a 4 GW scenario could imply something like $40 billion in annual revenue. At a 25% operating margin, that would mean $10 billion in EBIT. Put the same 16x EV/EBIT multiple on that, and Nebius could end up with a valuation of $160 billion. Against today’s roughly $57 billion market cap, that points to a potential tripling of the stock price, sending it to around $600.

Let’s be clear: that’s not my base-case forecast. And there are plenty of ways for things to go wrong – scaling, planning, financing, and potential share dilution, to name just a few.

Still, it’s hard to ignore the shape you see on Nebius’s stock chart.

Its shares jumped about 10% at the end of May after a regulatory filing showed that Situational Awareness, an AI hedge fund run by a former OpenAI employee, had bought a 5.6% stake in Nebius. The news gave Nebius a little more sparkle. After all, the fund has already backed a few big AI winners, including Bloom Energy and Sandisk. And now Nebius is its biggest holding.

Harmonic Drive

Harmonic Drive saw a 49% rally in May, fresh off a late-April upward revision to its profit. But even I was surprised by the strength of the rally.

In May, the company said it expects operating profit of 6.2 billion yen ($39 million) for the fiscal year ending in March 2027. That was below what analysts were expecting, although Harmonic Drive is usually conservative with its forecasts, so I wouldn’t make too much of that on its own. What stood out more was where the demand was coming from: orders linked to the sexier humanoid trend had picked up only slightly. The bulk of the growth came from semiconductor production instead.

The Tokyo-based Harmonic Drive also announced a new medium-term plan, targeting sales of at least 100 billion yen and an operating profit margin of 15%, resulting in 15 billion yen in operating profit by March 2031. That sounds nice. But the firm failed to achieve anything close to success on the previous plan, so you’ll want to take these new goals with a healthy pinch of salt.

With those numbers, the stock would still be trading at roughly a 60x price-to-earnings ratio – in other words, not cheap. In a way, that’s not new: Harmonic Drive has always traded for more than much of the sector because investors have been willing to shell out for its unique potential in robotics and automation.

That said, I don’t think the May update fully justifies the size of the rally. But I’m keeping the stock in the Finimize Portfolio because of its growth potential and the fact that it’s still one of the best publicly traded stocks for exposure to humanoids.

Korea’s memory-chip makers

Korea’s stock market also kept moving higher, powered by Samsung Electronics and SK Hynix, its two memory-chip giants. Together, they make up more than 50% of the main Kospi stock index, so when they move, the whole market feels it.

The Franklin Korea ETF has more than doubled this year. That said, those memory giants are still weirdly cheap, as I explained a few weeks back.

The core idea is that memory chips used to be a brutally boom-and-bust industry. Demand would rise and fall with PC and smartphone sales. It was famously exciting to watch, but scary to hold.

AI appears to be creating a much more durable boom. Over the weekend, investment bank Goldman Sachs moved its profit estimates sharply higher for 2027 and 2028 for Samsung and SK Hynix both, pricing in real, structural growth – or at least a much longer-than-normal boom-bust cycle.

The “Strait” play

My new idea this month was the Hormuz Recovery Basket. I picked eight companies whose shares have been hit hard by higher energy prices and higher interest rates.