Harrow In Sharp Focus: This Fast-Growing Pharma Stock Just Got Cheaper

This eye-care pharma specialist’s stock has dropped sharply in the past few weeks. And that caught Russell’s eye.

Healthcare investing is often about the big breakthroughs and blockbuster drugs. But some of the best opportunities come from smaller firms with profitable niches.

Harrow is one of those.

This ophthalmology pharma company is a name I’ve been (ahem) keeping an eye on for a while now. The business has always seemed promising, but the stock had run up so quickly that it was hard to justify buying in.

Recently, though, the picture has shifted a little. The stock price has fallen by 30% in the past few weeks, but the company’s growth outlook has stayed strong. And even after the pullback, Harrow’s stock is still up 400% over the past five years, compared with roughly 70% for the S&P 500.

That combination – a niche market, robust growth, and a recent selloff – makes this a good moment to take a closer look at the company and its prospects.

Part 1: What’s Harrow’s story and its growth strategy?

The company got its start in 2011, when CEO Mark Baum swung open the doors under a different name: Imprimis Pharmaceuticals. Over the next few years, the company expanded and evolved enough that the name no longer fit. So it was rebranded as Harrow Health, reflecting its new status as a more diversified healthcare holding company, with ImprimisRx and other subsidiaries under the broader Harrow umbrella. In 2023, the name was shortened to Harrow Inc.

And the company’s strategy has unfolded along the way, mostly across three stages.

Stage 1: Compound drugs. Its first revenues came along in 2014, with its ImprimisRx brand. The product was a compounded injectable steroid and antibiotic. Compounded medicine basically means a pharmacist or doctor has custom-prepared a drug by mixing or adjusting ingredients to meet an individual patient’s needs – like tailoring a suit, instead of buying one off the rack.

As demand for those kinds of treatments started to grow, Baum saw an opportunity to build his Tennessee-based firm into something bigger: a national ophthalmic pharmaceutical compounding company.

All of Harrow’s compounded products are manufactured at its facility in Ledgewood, New Jersey, and are licensed in all 50 states and registered with – and inspected by – the Food and Drug Administration (FDA) and the Drug Enforcement Administration (DEA).

The cash that started flowing from this compounding business gave Harrow the resources to try something interesting. Instead of spending heavily on in-house research, it began seeding new drug-development subsidiaries – companies like Eton Pharmaceuticals, Surface Ophthalmics, and Melt Pharmaceuticals. Once those businesses had gained traction, Harrow spun them out as independent companies, which enabled them to raise their own financing. It actually bought back ownership in Melt last November, seeing serious upside potential in the pharma firm, which makes a non-opioid sedative used in cataract surgeries and other procedures.

Stage 2: Branded drugs. By the late 2010s, Harrow began to pivot toward branded eye-care medicines, which have much higher margins than compounded ones. The idea was pragmatic: instead of pouring money into early research, Harrow looks for FDA-approved or late-stage drugs that bigger pharmaceutical companies have decided aren’t core to their strategy anymore. And that creates an opportunity for Harrow to step in, buy the products, and build a commercial business around them.

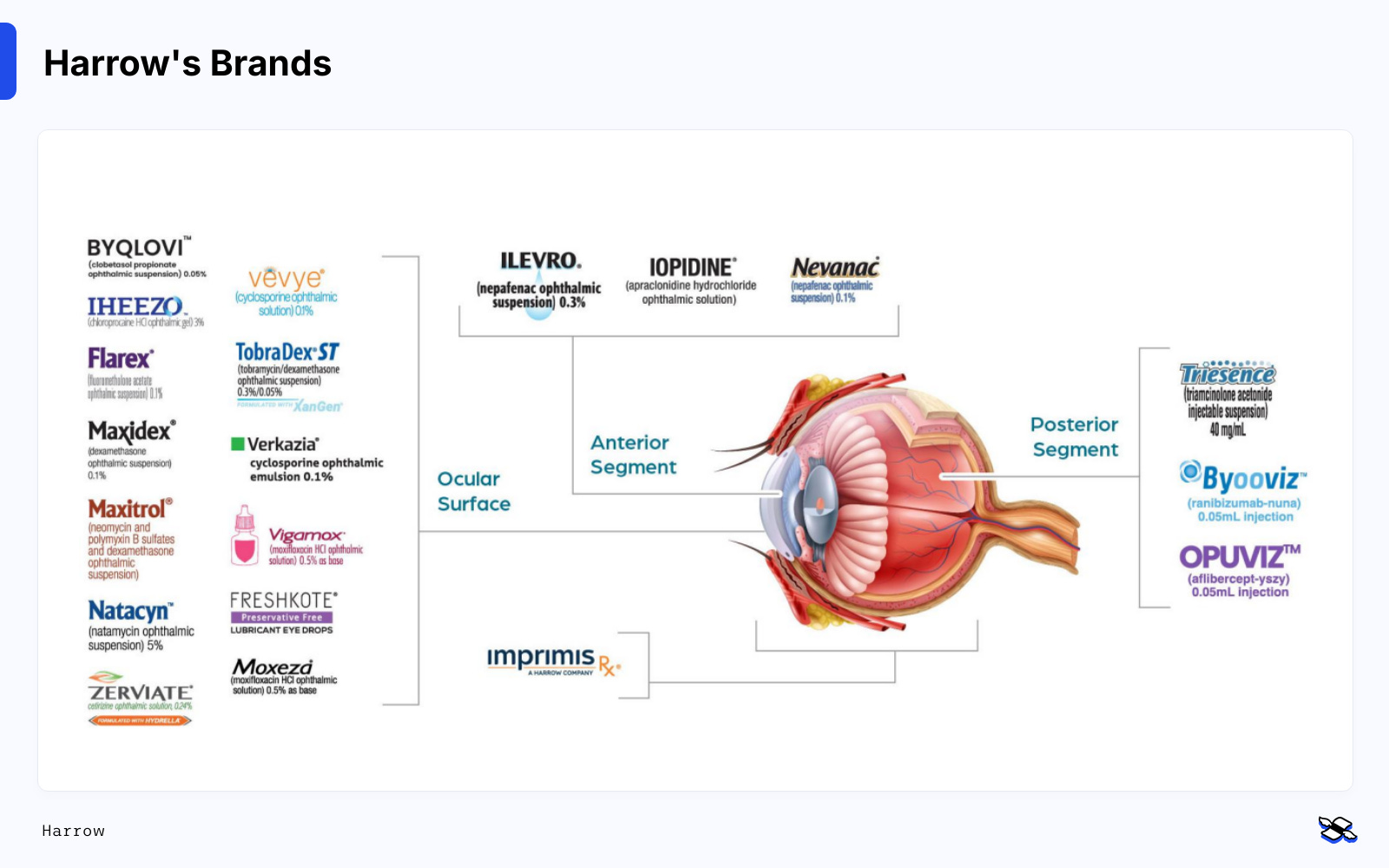

That’s what Harrow’s done. Through a series of acquisitions, it’s built one of the biggest ophthalmic drug portfolios, spanning multiple delivery methods – including eye‑drop solutions, suspensions, injectables, and sublingual (under the tongue) treatments. Those meds target a range of conditions like dry eye, age-related macular degeneration, cataracts, refractive errors, and glaucoma.

Harrow’s brands, as of March 2026. Source: Harrow.

Harrow has typically paid an upfront fee and sometimes royalties based on sales volume, as well. Then it plugs the acquired drugs straight into its existing infrastructure. The company has specialized sales teams that focus on specific customer groups: ophthalmologists, retina specialists, and cataract surgeons. This whole approach is basically a “buy and build” strategy.

Access and affordability are key here. The company runs its own in‑house support system called Harrow Access and Harrow Access for All, which helps smooth out insurance approvals and reimbursement. For patients who qualify, the program can also cap costs so treatments are affordable.